How State Loan Guarantees Can Improve Bank Lending Standards

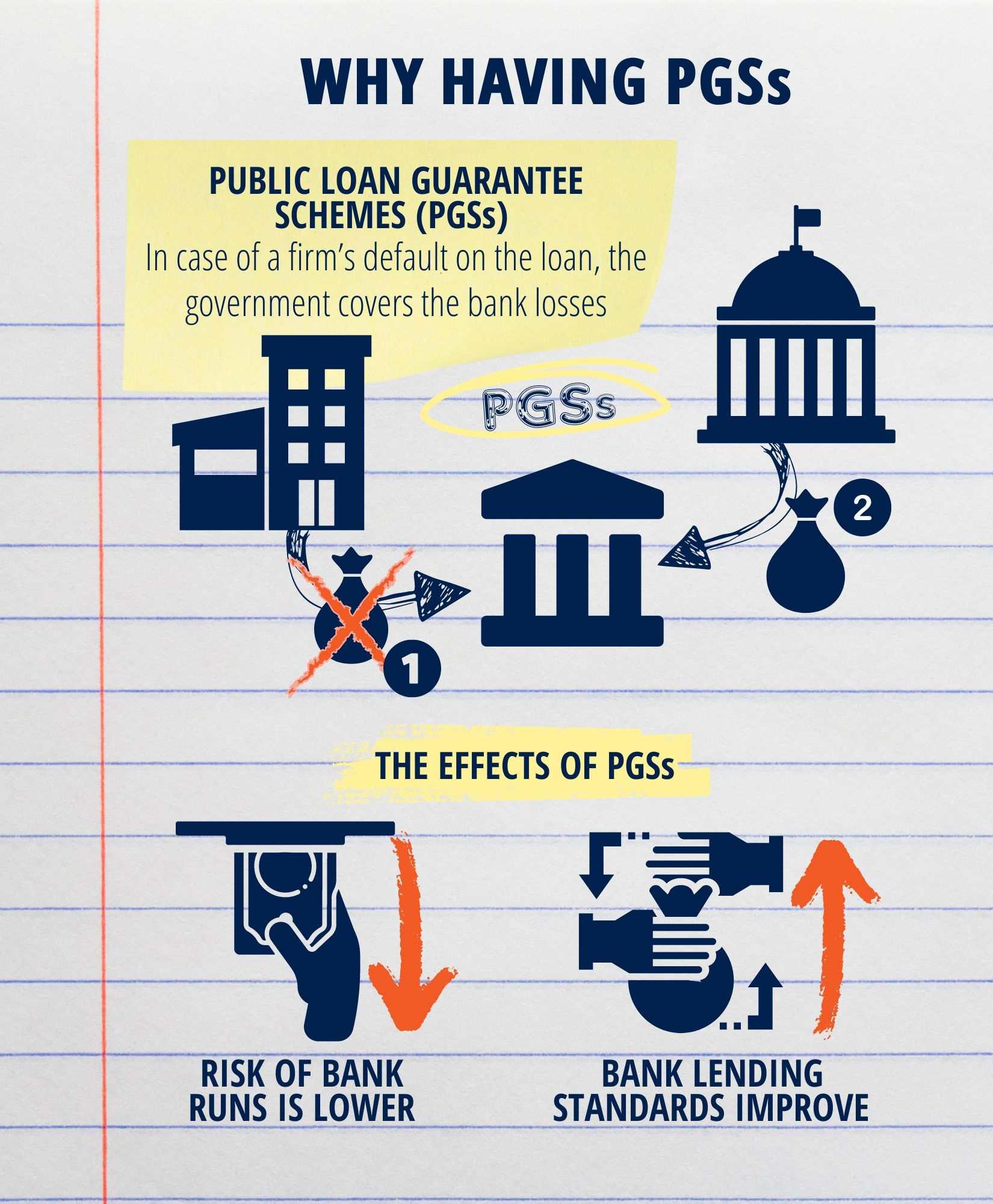

Public loan guarantee schemes (PGSs) are a tool that governments use to improve access to credit for sectors of the economy that would otherwise have difficulties in borrowing money. The ultimate goal is often to support output and employment. The concept is simple: in case of a firm's default on the loan, the government covers some (or all) of the bank losses, thus making the loan more attractive for banks, especially during times of uncertainty. While common even during normal times, their usage was extensive as a response to the 2020 Covid pandemic outbreak. More than 320 billion euros of loans backed by PGSs were extended in only four European countries as of September 2020.

In a recent paper, Elena Carletti (Department of Finance, Bocconi), Agnese Leonello (ECB) and Robert Marquez (UC Davis) built a model to study the effect of loan guarantees on depositor runs and bank lending standards. They found that, when PGSs are in place, the risk of bank runs is lower, whereas bank lending standards improve (credit institutions conduct more careful loan application screening) in all but the less capitalized banks.

Infographic by Weiwei Chen

In the authors' framework, well capitalized banks are susceptible to runs only when fundamentals (i.e. the economy) worsen. Whereas, banks with lower levels of capital can, in addition, suffer panic runs, when depositors withdraw their money because they fear that, if other depositors run, the bank may be unable to return their capital. Guarantees lower the incentive to run on all banks, independently of the capitalization level. The reason is that, if a loan is backed by a safer counterpart (like a State), the risk that a bank won't be able to repay its depositors is lower. This, of course, translates into greater financial stability.

What is perhaps more surprising is the effect of guarantees on a bank's underwriting effort. Indeed, one would expect banks to be less careful in deciding whom they grant loans to if some other entity stands ready to compensate their losses in the case of default. But instead, the authors show that when a PGS is in place, banks not only lose less money in case of default, but also stand to gain more if a loan does not default. Since the latter effect is stronger than the former, banks will exert more screening effort on loan applications, and the overall quality of their portfolio will increase.

There is one caveat, though. Loan guarantees are found to increase evergreening, i.e. inefficient loan continuation, meaning that banks do not liquidate a loan when it would be efficient to do so. The reason is that the risk of bank runs counterbalances banks incentive to continue inefficient loans. Since guarantees decrease the risk of runs, this effect is less strong and evergreening increases. Worse-capitalized banks are found to be more susceptible to this negative effect of PGSs.

"One key result is that it is not the 'shape' of the PGS that matters towards financial stability," said Professor Carletti, "but rather the existence of the scheme itself. Fine tuning the guarantees is less important than actually having one. A possible extension of our work could be to take a look at the other side of the guarantee, to see the effects on output and the cost of different schemes for the government."

Elena Carletti, Agnese Leonello, Robert Marquez, "Loan Guarantees, Bank Underwriting Policies and Financial Fragility", Journal of Financial Economics, Volume 149, Issue 2, August 2023, Pages 260-295, DOI: https://doi.org/10.1016/j.jfineco.2023.04.013.